Today's construction and field service industries are behind the ball if they're not using a mobile time tracking solution. Experts have repeatedly found that any business that isn't adopting technology, is sure to be left behind.

Whether for short- or long-term growth, investing in digitization and technology is what helps business owners stay competitive, according to McKinsey. While investing in technology like CAD or BIM are important considerations, mobile time tracking will also help you nip labor costs in the bud.

A dynamic, cloud-based solution will not only help save a ton of time and money on labor costs but will also help you boost productivity, improve customer service, get organized, and grow with you.

But with so many choices out there for mobile time tracking, it can be challenging to determine which one's best for you. Not all will suit your business so we broke down the top six mobile time tracking apps for construction so you can compare for yourself.

ClockShark

ClockShark is an award-winning, international time tracking solution that provides a powerful set of tools for construction and field service companies. From mobile time tracking and GPS tracking, to dynamic reporting and improved communications, this cloud-based platform continues to add new features to help manage projects and crews.

The Pros...

Built by contractors, for contractors.

Fast, easy setup with 5-star customer support.

ClockShark regularly improves its platform with upgrades and additions based on customer feedback.

The Cons...

Not customizable.

Smartphone required for mobile time tracking.

Specialized for construction/trades and field services (not best suited for other industries).

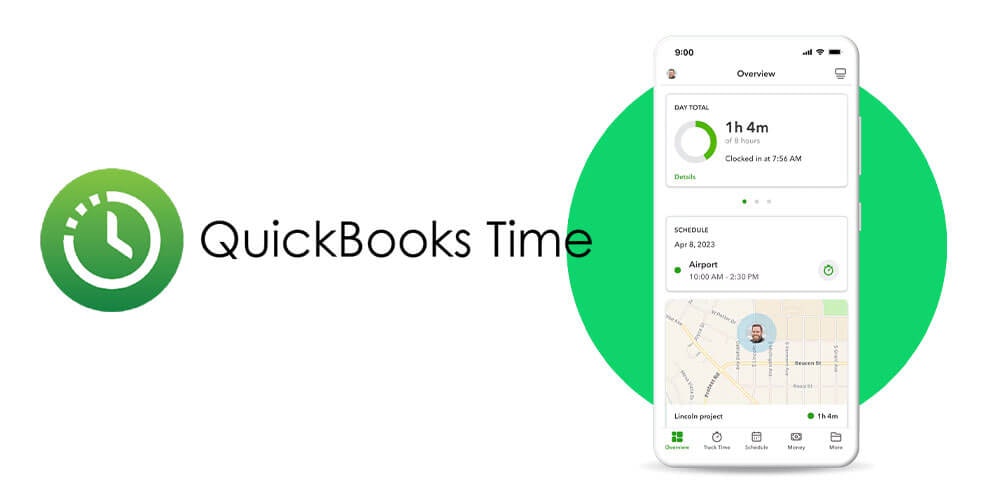

QuickBooks Time

QuickBooks Time is a popular time tracking software that many different companies use. It offers mobile time tracking for workers in the field as well as a desktop app for office workers. It integrates with multiple accounting programs to help you streamline your payroll and accounting processes.

It provides detailed reports and helps you manage your projects with team management features. It works on smartphones, tablets, and desktop computers and can be used as a kiosk clock for entire crews. You can also use their geofencing to ensure employees clock in and out as they enter a certain area and GPS tracking to know where your people are during their shifts.

The Pros…

QuickBooks Time can handle very large companies so if you have a large number of employees, QuickBooks Time’s platform is pretty good.

They have detailed reports so you can pinpoint problem areas and capitalize on positives.

QuickBooks Time comes with multiple integrations that make your payroll process much faster and easier.

The Cons…

QuickBooks Time is more expensive than similar platforms.

QuickBooks Time is owned by Intuit which is a huge corporation so you may not get the same kind of treatment you might get from another platform.

QuickBooks Time claims to provide “free” time tracking but it is not a completely honest statement. While they will let you try the software free for 14 days, they do not have a free version.

BusyBusy

Also geared towards construction professionals, BusyBusy offers mobile time tracking with helpful features like kiosk clock, scheduling, reports, and more. BusyBusy offers a free version and is easy to use.

Pros…

BusyBusy offers a free version that comes with the basic functions for time tracking.

Easy-to-use equipment tracking.

Employees can digitally sign their timecards.

Cons…

Limited integrations.

Not as customizable as other alternatives.

ExakTime

For construction companies, ExakTime is a popular choice for things like time tracking, scheduling, and GPS tracking. It is particularly geared towards the construction industry and has some integrations with popular accounting software like ADP, Sage, and QuickBooks.

The Pros…

No more paper timesheets. Timecards can be printed out easily to review.

Multiple integrations help to streamline your payroll process.

Easy to use.

The Cons...

Once you sign up, you’re locked in for a year.

There is a $1,000 implementation fee.

Learn more about ExakTime alternative.

Boomr

Boomr is also a construction-specific time tracking solution. It provides helpful reminders for employees to clock in and out, and administrative solutions that help streamline workflows and save time. With project tracking and shift management, it’s an ideal choice for a lot of construction companies.

The Pros…

Specifically geared towards construction companies.

Multiple integrations with accounting software.

Clean, user-friendly appearance.

The Cons…

More expensive than similar products.

Lacks helpful features like scheduling and job costing.

Limited integrations.

Clockify

For a free time tracking solution, Clockify is a very popular choice. With the free version, users can benefit from unlimited time tracking, reporting, support, and more. The program features colorful reports that help you stay organized and on top of your projects.

The Pros…

The free version works well for basic time tracking needs (and it really is free).

Helpful for tracking the money spent on projects.

Editable timesheets.

The Cons…

More complicated (less user-friendly) than similar products.

Paid plans are more expensive than similar products.

The Mac version is reported to be quite buggy.

Benefits of Mobile Time Tracking for Accountants and Bookkeepers

One of the shortcomings of traditional timekeeping is the potential for errors as well as inaccurate and mismanaged timesheets. With time tracking for accountants and bookkeepers, you can use an electronic timesheet to help increase profitability.

How does it assist with this exactly? The following ways:

Reduces employee time theft

With a mobile time clock, your employee gets credit for the time they were available and working — not a second more or less.

Improves employee accountability

Some employees forget to clock in and out. Mobile time tracking makes it easier for them to do so and makes it more likely they'll be able to do.

Eliminates any missed paper timesheets

Paper timesheets can easily get lost or misplaced. With mobile time tracking, there's no hard copy to retrieve. All the data is saved within the system.

Time clock allows for more accurate timesheets and discourages poor timekeeping by your employees. This will increase your organization's bottom line while making it easier for your team to do a better job managing their timekeeping.

How mobile time tracking improves your workflows

Improve productivity

When your employees use the right mobile time tracking app, it allows them to see a visual representation of how many hours they've dedicated to their role. It also allows them to see how much time is needed to complete a shift.

This promotes a feeling of transparency between the employer and employee. When they can see their hours represented, they understand that they're receiving credit for the hours they've worked. They can also see that their hours are correct and fair. The number of hours that they've worked and that the employer is crediting them for is 100% out in the open on a platform that both the employer and employee can view.

Every employee wants to be treated fairly while receiving the proper credit for their hard work. Mobile time tracking reminds them that they're receiving that credit. In turn, they'll feel valued and will be more productive in their positions while they fulfill their role.

Easy reports and job costing

Another feature of mobile time tracking is that it easily produces reports with information on the hours dedicated to each specific project. This enables your team to analyze the amount of labor going into each task. This helps with reviewing your organization's spending in one area and helps you adjust your budget as needed based on the hours logged. This is much more difficult to do using traditional timesheets. A mobile time tracking app can generate information on what each specific job costs to your team, specifically, aiding your planning efforts.

So much of your planning depends on knowing the cost of each project you're involved in. Imagine having a tool that gives you that information to make your financial forecasts going forward all the more reliable.

Payroll software integration

Aligning time tracking with your payroll is another way to streamline your accounting business operations. Being able to sync your time tracking platform with your payroll is a near necessity — it ensures all data from one program flows seamlessly to the other.

With traditional time tracking methods, the transition from the time tracker platform to payroll software is manual. Your staff will need to input the information. This increases the chances for potential errors. You're essentially counting on your staff to enter all timekeeping information 100% accurately. That's too big an ask for anyone. Any mistakes could lead to payroll issues — incorrect amounts on checks or incorrect hours reported on a particular project.

With payroll software integration, you're taking this out of the hands of your team and into the hands of your time tracking app and payroll software. Once you have these two platforms aligned, the entire process is automated. That cuts down on human error and increases the likelihood that all payments will be made in full, on time, and 100% accurately.

Save Time and Money with ClockShark

Employee scheduling

Another important component for accounting and bookkeeping companies to keep track of is scheduling. When you're juggling multiple projects, it can get easy for your employees to get overwhelmed. They can also lose track of what they're working on and when. With traditional time tracking, there's the possibility that your team will account for its time incorrectly. This can throw off your expectations for how to assign your team members to projects going forward.

With the increased oversight mobile time tracking gives you into what employees are working on which projects and clients, you'll have a better idea of how to schedule time in the future. It ensures you have your team dedicating the right number of hours in the right places. This also helps your employees in that when they're scheduled correctly; they don't have to worry about adjusting those schedules during the pay period. The baseline number of hours for each project is set and will not need to be altered due to the data your time tracker app has given you.

Scheduling your employees can be a daunting task, but a mobile time tracking provides you with the data you need to do it more reliably.

Conclusion

Finding a time tracking solution is easy to do. Finding the right time tracking solution is the trick to making it a successful transition to digitizing your company for growth. Make sure to do your own research to discover which one is right for you and your employees.

For a visual breakdown of these comparisons, you can view our comparison chart, here.